The Role of Insurance in Plumbing: A Homeowner’s Guide

The role of insurance in plumbing is to protect homeowners and landlords from the financial fallout of water damage, faulty workmanship, and on-site accidents. Plumbing liability insurance, the industry’s standard term for this protection, covers everything from a burst pipe that floods your kitchen to a worker injured on your property. Without it, you absorb those costs directly. Water damage is the single most costly claim for plumbing contractors, often exceeding $12,000 per incident. That number alone explains why verifying a plumber’s coverage before any work begins is one of the most practical things you can do as a property owner.

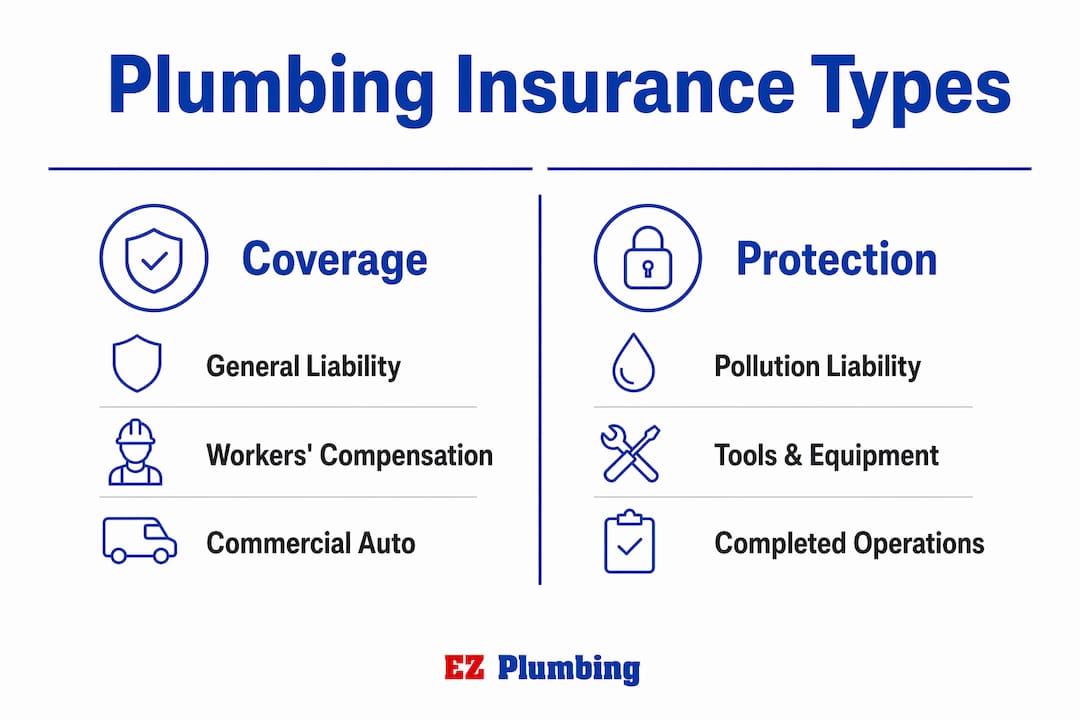

What are the main types of plumbing insurance coverage?

Plumbing insurance is not a single policy. It is a collection of coverage types, each addressing a different category of risk. Understanding what each one covers tells you exactly what you are protected against when you hire a plumber.

General Liability Insurance is the foundation. It covers property damage and bodily injury caused by a plumber’s work on your property. If a plumber accidentally cracks a water main and floods your basement, general liability pays for the repair and cleanup. This is the minimum coverage you should require from any contractor you hire.

Workers’ Compensation Insurance covers injuries to the plumber’s employees while they work on your property. Most U.S. states require plumbing companies with employees to carry this coverage, with premiums averaging $3.50–$7.00 per $100 of payroll. Without it, an injured worker could potentially pursue a claim against your property.

Pollution Liability Insurance addresses a risk most homeowners overlook entirely. Standard general liability policies exclude pollution-related claims like sewage backups and mold contamination. A separate pollution liability endorsement, which typically costs $500–$3,000 annually, fills that gap. If a sewer line repair goes wrong and raw sewage backs up into your home, this is the coverage that pays.

Commercial Auto Insurance covers the plumber’s service vehicles. If a plumbing van damages your property while on site, this policy responds.

Tools and Equipment (Inland Marine) Insurance protects the plumber’s gear. Expensive plumbing tools like pipe cameras and hydro-jetting equipment are often overlooked in standard policies. If a plumber’s tools are stolen from your driveway during a job, inland marine coverage prevents the plumber from cutting corners by using inferior replacement equipment.

| Coverage Type | What It Protects Against |

|---|---|

| General Liability | Property damage and bodily injury from plumbing work |

| Workers’ Compensation | Employee injuries on your property |

| Pollution Liability | Sewage backup, mold, and contamination claims |

| Commercial Auto | Damage caused by service vehicles |

| Tools and Equipment | Theft or damage to plumbing tools and gear |

Pro Tip: Always ask for a Certificate of Insurance, not just a verbal confirmation. A certificate lists the policy numbers, coverage limits, and expiration dates for every active policy the plumber carries.

Why does plumbing insurance matter when you hire a plumber?

Hiring an uninsured or underinsured plumber transfers financial risk directly to you. That is the core issue. A plumbing error that causes water damage to your walls, flooring, or electrical systems can easily cost tens of thousands of dollars to repair. If the plumber carries no insurance, you pay for it.

The risk does not end when the plumber leaves. Completed Operations coverage protects you against damages that appear after the work is finished, sometimes months later. A faulty pipe joint installed today might not fail until next winter. Completed Operations coverage responds to exactly that scenario, covering the resulting damage even after the contractor has been paid and moved on.

Landlords face compounded exposure. A plumbing failure in a rental property can displace tenants, trigger habitability claims, and generate repair costs all at once. If the plumber who caused the problem carries only minimum coverage, your own landlord policy absorbs the excess. That creates a gap that is entirely avoidable by verifying the plumber’s coverage upfront.

Hiring a licensed plumber with proper insurance is not just about peace of mind. It is a direct financial decision. The cost of verifying coverage is zero. The cost of skipping that step can be significant.

Pro Tip: Ask specifically whether the plumber’s general liability policy includes Completed Operations coverage. Many basic policies omit it, leaving you exposed to claims from work that fails weeks or months after completion.

Common insurance gaps that leave homeowners exposed

The most dangerous insurance gaps are the ones nobody mentions until a claim is denied. Standard general liability policies contain two exclusions that catch property owners off guard more than any other.

The first is the pollution exclusion. Most general liability policies treat sewage, mold, and chemical contamination as pollution. That means a sewage backup caused by a plumber’s error may not be covered under a standard policy. Standard policies exclude these claims unless the plumber carries a specific pollution liability endorsement. Always ask for proof of that endorsement before sewer line or drain work begins.

The second is the “your work” exclusion. This exclusion means the policy will not pay to repair or replace the plumber’s own faulty workmanship. If a plumber installs a water heater incorrectly and it fails, the policy does not cover the cost of replacing that water heater. It covers only the resulting damage to other property, such as water damage to your floors. Many homeowners assume insurance covers everything. It does not.

Many plumbers carry only minimum coverage required by law, which is often inadequate for latent defect claims. This is especially true for smaller operators working on high-value properties in Los Angeles.

For high-value properties, umbrella or excess liability insurance provides an additional layer of protection above the plumber’s base general liability limits. Umbrella insurance is cost-effective relative to the protection it adds, and it becomes critical when a single incident could generate a claim that exceeds standard policy limits.

One more gap worth knowing: XCU (Explosion, Collapse, Underground) hazard coverage is required for any plumbing work involving excavation. Without it, a claim from underground pipe work could be denied entirely.

How to verify adequate coverage before hiring a plumber

Verifying a plumber’s insurance takes less than ten minutes and protects you from significant financial exposure. The process is straightforward when you know what to ask for.

Request a current Certificate of Insurance before any work begins. The certificate should list the following active policies:

- General liability with a minimum $1,000,000 per occurrence limit

- Workers’ compensation if the plumber has employees

- Pollution liability endorsement for any sewer, drain, or water heater work

- Completed Operations coverage included within the general liability policy

- Commercial auto if service vehicles will be on your property

Ask the plumber directly whether their general liability policy includes Completed Operations and pollution liability. If they cannot answer clearly, ask for their insurance agent’s contact information and verify it yourself. A reputable plumber will not hesitate to provide this.

Plumbing warranties for homeowners work alongside insurance to provide layered protection. Insurance covers accidents and damage. Warranties cover defective workmanship. Both matter.

Insurance complements a strong risk management program but does not replace it. Selecting a licensed plumber, requiring permits for major work, and scheduling regular plumbing inspections all reduce the likelihood of a claim occurring in the first place. For landlords, this means building insurance verification into your standard contractor vetting process, not treating it as optional.

Pro Tip: For rental properties with multiple units, ask whether the plumber’s policy covers commercial work. Some residential-only policies exclude multi-unit buildings, which creates a coverage gap on the exact properties where plumbing failures are most disruptive.

Key Takeaways

Plumbing liability insurance is the primary financial safeguard between a plumbing failure and a costly out-of-pocket repair bill for homeowners and landlords.

| Point | Details |

|---|---|

| Verify before work starts | Always request a Certificate of Insurance listing all active policies before any plumber begins work. |

| Pollution coverage is separate | Standard general liability excludes sewage and mold claims; a pollution liability endorsement is required. |

| “Your work” exclusion limits coverage | Insurance covers resulting damage from faulty work, not the cost of redoing the faulty work itself. |

| Completed Operations protects you later | This coverage responds to plumbing failures that appear weeks or months after the job is finished. |

| Umbrella coverage fills high-value gaps | For high-value properties, excess liability insurance provides critical protection above standard policy limits. |

What I’ve learned from years of insured plumbing work

The biggest misconception I see from homeowners is that any insurance is enough insurance. A plumber who hands you a certificate with a general liability policy and nothing else is not fully covered for the work they are about to do on your property. Pollution liability and Completed Operations are not extras. They are the coverage types that actually respond when something goes wrong after the job is done.

The second thing I’ve observed is that insurance works best when it rarely needs to be used. At Ez-plumbing, we treat technical protocols, proper permitting, and camera inspections as the first line of defense. Insurance is the financial backstop when something unexpected happens despite doing everything right. A plumber who relies on insurance to cover sloppy work is not a plumber you want on your property.

My advice to every homeowner and landlord is this: ask for the certificate, read it, and call the insurance agent if anything is unclear. The plumbing insurance benefits you gain from that ten-minute verification are worth far more than the time it takes. And as your property ages or your plumbing needs grow more complex, revisit the coverage requirements. A repiping project carries different risks than a faucet replacement, and the insurance requirements should reflect that.

— EZ

Ez-plumbing’s fully insured plumbing services in Los Angeles

Ez-plumbing holds C-36 License #583868 and carries full insurance coverage, including general liability, workers’ compensation, and pollution liability, on every job we perform across the greater Los Angeles area. You never have to wonder whether you are protected when our team is on your property.

Whether you need a water heater installation backed by proper workmanship coverage, a sewer line inspection, or emergency plumbing service, Ez-plumbing brings licensed, insured professionals to every call. Our coverage protects you against property damage, on-site injuries, and latent defects. Contact Ez-plumbing today to confirm our current insurance certificates or to schedule service. We are code-compliant with LA municipal requirements and ready to provide proof of coverage before any work begins.

FAQ

What does plumbing liability insurance actually cover?

Plumbing liability insurance covers property damage and bodily injury caused by a plumber’s work, including water damage to floors, walls, and fixtures. It does not cover the cost of redoing the plumber’s own faulty workmanship.

Does every plumber need to carry workers’ compensation?

Most U.S. states require workers’ compensation for plumbing companies with employees, with non-compliance resulting in heavy fines and personal liability exposure for the contractor.

What is Completed Operations coverage in plumbing?

Completed Operations coverage protects property owners against plumbing failures that occur after the job is finished, sometimes months later, such as a pipe joint that fails weeks after installation.

Why doesn’t standard general liability cover sewage backups?

Standard general liability policies treat sewage and mold as pollution and exclude those claims by default. A separate pollution liability endorsement is required to cover sewage backup and contamination damage.

How do I verify a plumber’s insurance before hiring them?

Request a current Certificate of Insurance listing general liability, workers’ compensation, pollution liability, and Completed Operations coverage, then call the listed insurance agent to confirm the policies are active.